- cross-posted to:

- personalfinance@lemmy.ml

- cross-posted to:

- personalfinance@lemmy.ml

You must log in or # to comment.

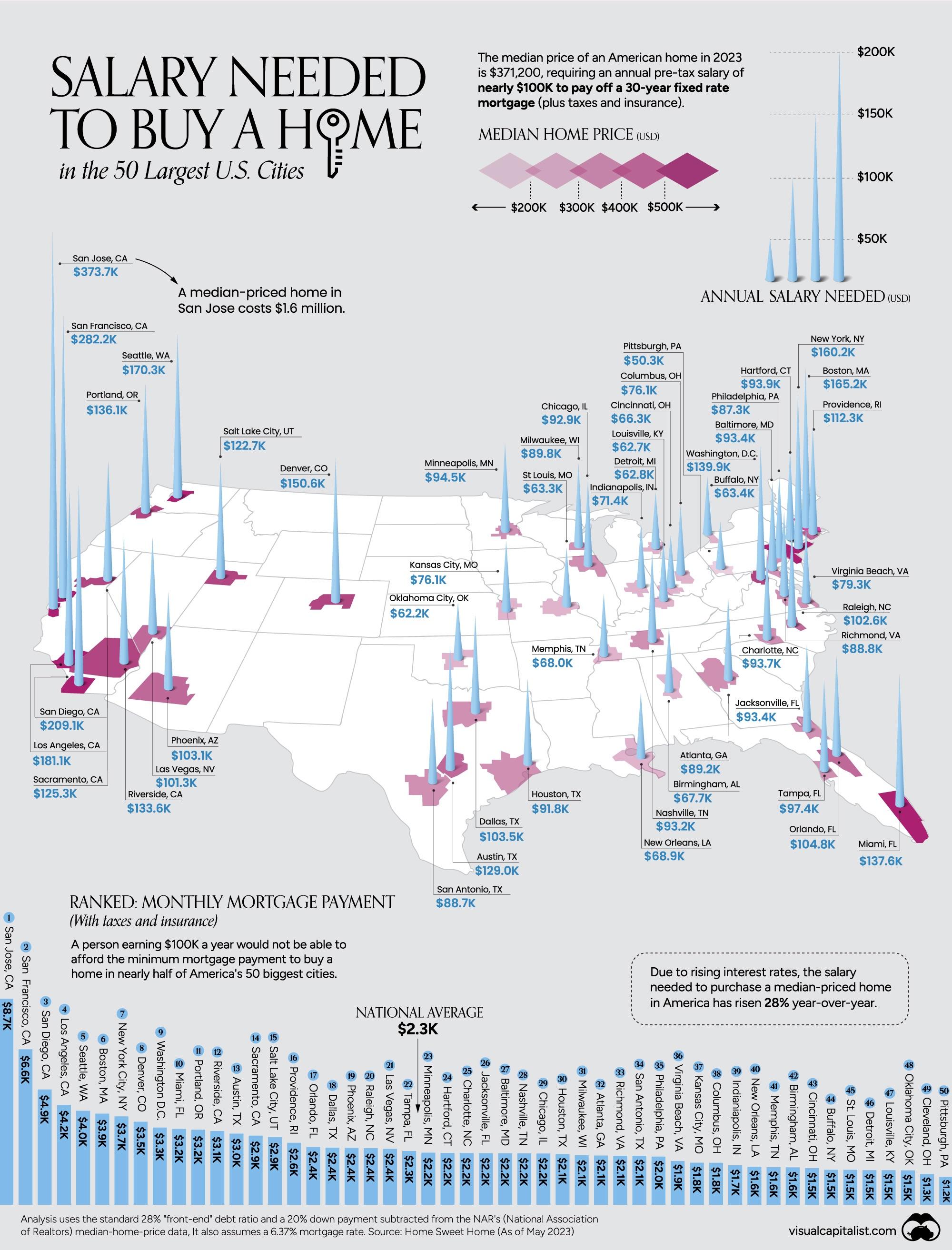

20% down payment is ridiculous these days. For the median home of 370k that’s 74k you need to have lying around.

Double that for Canada

$2,172,613 ($1,586,224.75 USD) if you want a detached in the Vancouver area

Condos bring the average down as they only cost $816,356 ($596,021.52 USD) which is pretty affordable as far as housing is concerned around the city

Good thing wages have kept up with house prices right?

Right?!

Detached homes shouldn’t even exist in Vancouver metrocore anymore so, it makes sense to be a fortune

It was the Vancouver area so it includes the surrounding areas but you are correct

Yeah, I know. It goes from “impossible luxury” to “barely affordable” as you go from downtown towards the edges of the metro region. Just saying that it’s not surprising for Vancouver that those prices are so jacked up.

It may surprise those who don’t live here that 80% of Vancouver proper looks like a sleepy suburb of detached single family homes. It is mostly detached homes here. Even a townhouse can take a decade to build due to NIMBYs.

It’s not an enormous hurdle for folk that already own a home, but it creates a huge barrier to entry. You can get in for less but then you get to waste obscene amounts of money on PMI. Literally just throwing money into someone else’s pocket for no return.

West coast is so fucked.

You need more than 180k to buy a home in LA too. Maybe if you are married and both make over 140k then you can actually afford an 800k condo.

Glad I got my house two years ago. I was hesitant at the time because houses were going so fast you barely had time to think about it, get second opinions, or really anything.

At this rate, we will see the exact same comment in two years.

My wife and I bought our house two years ago too. The market around here has gone utterly bonkers since. If we had tried to save up a while longer like we were originally planning to we would never have gotten there.

Get in line, Salary. We’re all trying to survive this market, and we were here first. ☝🏽

And that’s just to pay the mortgage, never mind things like food or saving to retire or even the 20% down payment the graphic assumes that you’ve made.

There must be something wrong with the math that they used here, because I’m familiar with a few of these markets and have a higher salary than what is listed and definetely couldn’t buy a house in those markets without it being more expensive than would be responsible - both in terms of down payment and monthly cost

For example, I think you’d need a lot more than 180k to buy a house in LA

It’s possible they’re including buyable apartments as well as single family houses but 180k still sounds WAY too low for LA

Yeah that could be it, or maybe they’re doing the math as literally “is your monthly take home less than the cost of the monthly payments”. In which case I could see 180 qualifying, but that isn’t how any sane person would define affordability lol

Same with San Jose. 1.6m will get you a 1bd apartment. A 3-4 bd house will run you at least 2.5m

As a European, at first I thought this showed house prices, and not yearly salary required to buy a house and thought: “well, that’s not too bad …”, but oof!

When does this bubble pop?

That’s the fun part about this specific market, it isn’t a bubble that can pop. The people that caused this issue had the money to buy the houses they did. This is just the new normal, and the best part about that is that house prices only ever go up!

Yay! I can’t wait until the absolute garbage dilapidated pile of shit in the worst parts of town and a flood zone go from 300k now to 500k or more! It’s going to be so fun to see houses that I’d never in a million years want to live in, sell for hundreds of thousands above what I could afford anyway.

The argument from asshats with no empathy used to be: so move to a LCOL area (ignoring that work cant be found there.) Well even ignoring the work issue, those dont exist anymore. The WFH “movement” gave people the freedom to move to those LCOL areas so now they aren’t low cost anymore.

I can’t even leave the expensive shit hole area I live in because everywhere else is too expensive with less job opportunities… The future is so fun!

/wrist.

I don’t know how accurate it might be but I heard of a theory recently for the US that the recent reversal where students will be required to repay their loans in full is going to tank the housing market because a large chunk of people from the very demographic that would normally be first-time buyers won’t be able to afford to buy. There were supposed to be a bunch of cascading effects from this, but I’m sorry I can’t remember further details now.

Loan repayments resumed yesterday for over 100 million Americans. Now there are a lot of different options especially their income-driven ‘SAVE’ plan which calculates repayments based on earnings. So for me who’s struggling between jobs, I don’t have to pay jack until they see reported income luckily.

But the housing market here in Midwest US doesn’t seem like it’s changing for the better anytime soon. Median Housing cost is like triple average yearly salary, and on top of that our taxes are just abhorrent.

Also in the fun struggle to find long term domicile here. One thing I’ve been running numbers is just straight up building new houses. Many states building is cheaper than buying; disregarding zoning and permits.

I’m hoping with new remote work abilities that in the future I can caravan with other like-minded Gen-z/millennials to some unincorporated stretch of rural land and just set up a new town, wild West style.

Seattle is less affordable than it seems. Unlike California and many other states, WA has neither a property tax increase limit nor a homestead exemption. As a result, property taxes in WA, already some of the highest in the country, arbitrarily track market prices and don’t get any kind of tax break. My property taxes cost more than my 30yr fixed mortgage now. If the price trends continue, I won’t be able to afford my house within a decade, just because on paper someone might theoretically be willing to pay some ridiculous amount to buy it from me.

Huh, I could afford to live in buffalo. That’d be nice if it wasn’t buffalo

This is from the 80s right? The price in my area is not even close

It’s not house prices it’s annual income required to buy.

Oh ok totally misread that

Is that a new sentinel returns map ?

{kind=link}