dj_voight_kampff [he/him]

You really didn’t think it would be that easy to reject universal love, did you?

- 16 Posts

- 14 Comments

Joined 28 days ago

Cake day: October 2nd, 2024

You are not logged in. If you use a Fediverse account that is able to follow users, you can follow this user.

13·11 hours ago

13·11 hours ago

A group of women who were borrowers with the Grameen Bank

Mallika, a villager from Jobra explained the problems with the weekly repayments. She said, “I bought land with the money. But, then I found that I couldn’t earn that much money. I had spent the money. So I had to take a new loan to repay the old one.” Another villager Yasmeen said that the weekly payments forced her to take other loan. Eventually, she was indebted to five organizations. Other women who took loans, had to return to their local loan sharks in order to keep up with the weekly payments.

The group payments of these loans puts intense pressure on the borrowers to make their weekly payments because if one member of the group defaults, the other group members, who are in an equally precarious position, have to cover the defaulters loans. Therefore, the social pressure forces borrowers to use any means necessary, even local loan sharks, to find the necessary money to make these repayments, defeating the purpose of the Grameen Bank. Since the Grameen Bank was created to help borrowers not use usurious loan sharks.

This is no wonder, according to research done by QK Ahmed, 1189 of 2501 borrowers surveyed could not repay their loans on time. 72.3% of them had to take out other loans to make their payments. 10% had to sell assets that gave them productivity, like goats, in order to make their repayment. Another study sampled 1489 families from 15 villages. Only, 5-9% of the borrowers said they were better off after using micro-credit.

On top of the failures in helping their borrowers, Grameen Bank has also had serious issues with its corporate governance. Mohammed Yunus, the founder has been at the center of many scandals at the heart of his Grameen institutions, which forced him to resign in 2011. When Grameen Bank lost its tax exempt status, in 1998, he moved $100 million to another shell organization called Grameen Kalyan, and then loaned that money from Grameen Kalyan to Grameen Bank, in order to avoid paying taxes. His Grameen Yogurt business was found using adulterated milk in 2011.

Shortly before occupying his position as chief of Bangladesh, Mohammed Yunus was convicted of violating Bangladeshi labor laws with his other subsidiary Grameen Telecom. Bangladeshi law requires a company to pay five percent of its net profit to a welfare fund that could later be used for pensions. It seems that Grameen Telecom, in its haste to make profits, failed to create such a fund.

Despite, being disgraced and scandal plagued, he continued to be the object of praise and adulation in the West. He has been praised by the likes of Larry Summers and Bill Clinton simply because the Grameen Bank model perfectly fits in with the neoliberal consensus that the West hopes to impose upon the world.

Poverty in the third world is caused by underdevelopment and lack of societal infrastructure. Alleviating this poverty, which has been done successfully in China and Vietnam (to name a few), requires massive government intervention and government programs to change the situation. People in villages in Bangladesh are poor because there are no places for the masses to find decent paying jobs. That requires government investment to set up large scale industries that can employ thousands of semi-skilled workers to give them decent wages. In order to set up these industries, there needs to be large scale infrastructure investments in public roads and trains that will allow these goods to be moved efficiently.

The government also needs to invest in high-quality public schools to create a more skilled labor force for the next generation. On top of it, there needs to be social programs in healthcare and retirement such that one medical emergency doesn’t force a villager to sell her house.

Another Borrower from Grameen Bank in Jobra

But, since the 1970s, the Washington consensus managed by the dual institutions of the IMF and World Bank have been forcing third world countries, including Bangladesh to do the opposite. Since its independence, Bangladesh has been forced to:

[Dismantle big public enterprises.] Large mills were replaced by export processing zones, shopping malls, and real estate.

Export-oriented garment factories became the mainstay of manufacturing. Incidents like the Rana Plaza collapse in April 2013 showed the extent of cruelty and greed in these death traps.

Permanent jobs in factories were replaced by a system of temporary, part-time, outsourced, and insecure work.

The biggest source of foreign exchange has been remittances; existing side by side with a huge outflow of resources through the transfer pricing and profit outflow by foreign companies, and transfer of accumulated wealth by local business groups, legally and illegally.

The number of workers abroad is now more than the number of workers working in the country’s factories, who took this risky option because of job scarcity.

The feminization of the working class is another recent phenomenon, which happened because of a reduction of purchasing power and increase of job insecurity.

That has kept pressure on the families to work longer and to join the workforce with more than one family member, including children.

Energy resources and power have been systematically privatized. Power became a costly commodity and costs for the productive sector have increased, while energy security for the majority was threatened. All of this hurt the peasants; many had to join the labor market at home and abroad.

Land grabbing, occupying public spaces by private business, and deforestation have uprooted many. Rural branches of state-owned banks have closed down, squeezing the access to cheaper finance for rural people, and forcing them to go to microcredit, which has higher interest rates.

However, the philosophy of neoliberalism requires the government to keep a hands-off approach on all the infrastructure projects and social programs required for mass poverty eradication. The Grameen philosophy perfectly dovetails into the dastardly Washington Consensus. If poor people can be given enough loans and high interest rates, they can remove themselves from poverty. Anyone who fails this uphill battle, is at fault for not working hard enough to pull themselves up from their bootstraps.

As the new leader of Bangladesh, given his philosophy and closeness to the neoliberal institutions, it is unlikely that he will involve Bangladesh in large-scale projects with the Belt and Road initiative, which has been instrumental in developing much needed infrastructure in the most underdeveloped areas of the world. Instead, he is likely to follow Bangladesh into bigger and bigger macro-debt traps created by IMF and World Bank.

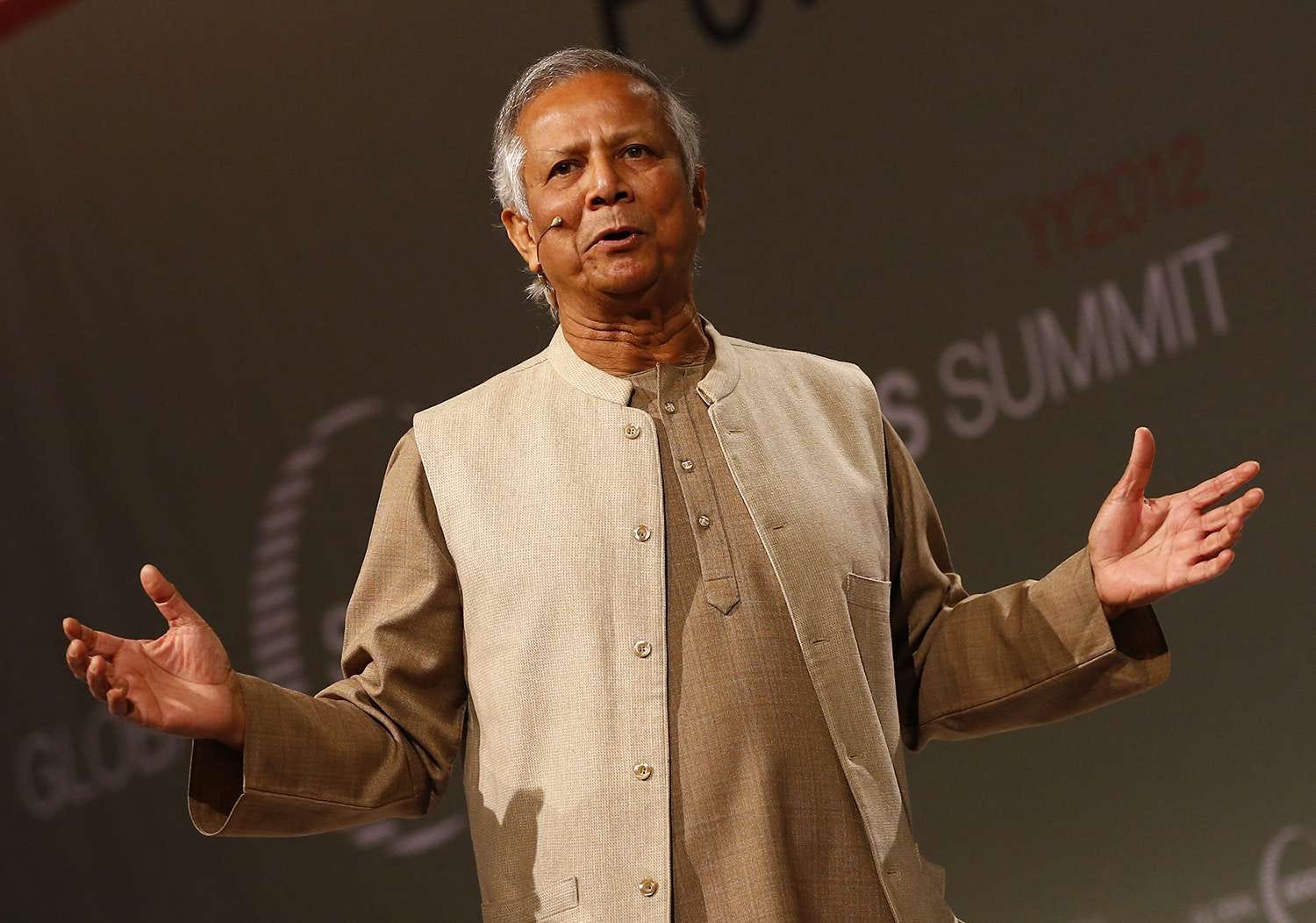

Mohammed Yunus at a Global Summit to spread his brand of propaganda

He will sweet talk on the importance of social responsibility while allowing big manufacturers to set up less than safe garment factories in Bangladesh, such as the one that collapsed in 2013. Most importantly, he will allow status quo to continue. This will allow him to be praised in the West as the new face of democracy in Bangladesh, regardless of the situation of the people within.

Yunus, Muhammad. 2003. Banker to the Poor: The Story of the Grameen Bank, p 69

Ibid, p 70

Bhel Puri is a street side snack made with puffed rice that is available throughout the subcontinent

According to the myth constructed by Mohammed Yunus himself, in 1974, he went to a house of a bamboo stool-maker Sofia Begum, in the village of Jobra. She had apparently borrowed money from the local loan sharks to get bamboos at usurious interest rates. She claimed the money lender charged 10% interest per week. After being moved by his experience, he allegedly gave her and another 42 villagers $27 which freed them from this perpetual state of bonded labor[1](javascript:void(0)).

Seeing the “success” of his loans, he reasoned that the families were poor, not because they didn’t have money (which is the obvious definitional cause of poverty), but they were poor because they did not have access to credit.

From this experience, his life mission was born. He was to ensure that every one would be able to get loans, regardless of how poor they were.

According to the Grameen Bank, this is how, a loan is supposed to operate in theory: If someone wants a loan, they have to form a group of five villagers. The loan is given to the group at 20% interest rate and each of the five members are responsible for the loan collectively.[2](javascript:void(0))

For example, if a group of five people borrow 1000 Takas, they will have to repay 20 Takas a week on the principle for fifty weeks. The 200 Takas of interest are due on a lump sum at the end.

The mythology is also combined with an intense propaganda effort. In 2006, in Germany, they staged a play called “Talisma and the Microcredit”:

The play was set in a remote village of Bangladesh, full of poor people and few landlords. Taslima, a poor girl, lived there with her parents. One day, a fully suited and booted World Bank consultant arrived with a “development” project to rescue the poor and make the village developed. After some time the World Bank project, as usual, created havoc—bringing more distress for the poor, more money for the rich, and intensifying natural disaster. The increasing floods and river erosion made Taslima’s family lose everything. At this point a miracle happened: Grameen SOS arrived. The poor villagers received information about microcredit, the way to prosperity and empowerment! Taslima and others formed a group to get microcredit, but since they only had four members, they needed one more to form a group eligible for a loan. In the meantime, the World Bank consultant realized his disastrous role, and after desperately looking for Taslima to begin a new life, he joined her, leaving his suited and booted world behind. They became five, allowing them to form a group to enter the microcredit world, and they lived happily ever after!

While in theory, it sounds like a great idea. People who are living on the edges of poverty can get over their problems by simply opening up a Bhel Puri stand in their villages, reality of these loans are a complete different matter.

A Danish documentary filmmaker went back to Jobra after the publication of the book and visit by none other than Hillary Clinton. In that village, 60 families took loans from the Grameen bank to build houses. Only 3 families succeeded and one of the families that did succeed had to sell their house because their daughter became ill and they needed money to pay for her appendix operation. Also, Sofia Begum, the woman whose situation started all this, died in abject poverty in 1998.

Despite, occasional success stories, the structure of the loans make it nearly impossible to do what the Grameen Bank claims it wants to help villagers do: start businesses. One week after they receive the loan, the villagers have to make their first repayment. Most people are not even able to get their businesses up and running within a week, let alone, generate enough cash to make repayments on these loans. When interviewing villagers, many repeated the same story. They had to take up other loans in order to make their weekly repayments.

The Mythology Behind the Grameen Bank

We look at the history of Bangladesh’s New Leader Mohammed Yunus

The day after the color revolution in Bangladesh, Mohammed Yunus, founder of the Grameen bank, a darling of the west, and a favorite of the Clinton foundation was coronated as “Chief advisor” to the new interim government. To understand the man, and how he will govern in Bangladesh, it is important to understand his history.

Before occupying his newest role as Bangladeshi Juan Guaido, Mohammed Yunus rose to fame in the 1990s, for his Grameen bank, a bank whose purpose was to give micro-loans to poor people. It eventually expanded to create a cottage industry with his Grameen Telecom, Grameen Fisheries, Grameen Danone Food and more!

In his effort to promote the Grameen Bank, Mohammed Yunus has made outrageous claims about his micro-loan program. He once said, “Poverty will be eradicated in a generation. Our children will have to go to a `poverty museum’ to see what all the fuss was about."

Even after 40 years of founding his ‘revolutionary’ institution, Bangladesh remains as poor as ever with 71.4% of the population living on less than $5.50 a day, while 1.3 million children are engaged in child labor. Sadly, people in Bangladesh experience poverty first-hand, and life, itself, is the poverty museum.

However, if we look at articles and literature on the Grameen Bank in the West, it mostly consists of hagiographies and repetition of outlandish claims made by Mohammed Yunus. A cursory examination proves that it is anything but a poverty relief program and the only thing these micro-loans guarantee is that their borrowers will take on more predatory loans.

The theory of micro-lending goes something like this: Give an impoverished, destitute villager 10,000 Takas as a loan. They will use that money to open up a Bhel Puri stand (or something similar), and then, with the income they generate from the Bhel Puri stand, they would not only repay the loan, but they will lift themselves out of poverty using their Bhel Puri straps.

I know that not taking prisoners encourages people to fight to the death, not denying that, it strikes me as a political dumb guy move like trying to use a surveillance device (cybertruck) as a technical. If I were to justify such a move I’d point out it’s discouraging further mercenary involvement, terrorizing people who would take up arms against them. ╾━╤デ╦︻( ͡° ͜ʖ├┬┴┬┴ᕕ( ᐛ )ᕗᕕ( ᐛ )ᕗ

Also, who said anything about expecting the same thing to happen to Russian troops? They already c̷̤͙̬͇̜͖͙̼̻̮̭͈͐̒̓̐͐̌̆̈́̊̀̒͑̚͟͠ͅö̸̧̖̺͇͈̥̜̟̘̪͇̗̫̝̽̅͛̀̍͘ỏ̷̬̙̲̯̞̬̂́̉̎̔͆͑̋k̵͔̥̲̼̓̓̇͠e̵̠͉͇͛̑̆̐͊͒d̴̺͉̳̯̦̮͕͎͖̺̔̀͘̚͜͜ ̴̛̝̠̥̋̽͆̾̽̐̄̌̃͒̿̀̕͝͝á̵̮̤͑̕͠ṋ̸̛̪̗̙͉̤̹̂̋̔̊̈́̋̂̆ͅd̸̡̗̦͇̟̥̐̇̋̈́͛̓͒͌͒͘̚͠ ̷͚̬̦̖̈́́͆̌̀̓̑͑͐͠ͅa̴̢̙͙̻̺̼̼̗̞̻͕̻̋̏̑̽͛̈́̈́̿̑̀̄̕͟͝ͅt̴̛̮̱̥̬͎͔̜̞̰͈̦͆̎͐̈́̃̒́̃͂͌̑e̴͖̙̮͉͙̐̉̈́́̂̊̍̂͡͠ ̶̻͆͑̇̏̈́͝ͅ someone?

For once I agree with a Southfront commenter (yes I read those no you shouldn’t) they should just declare them all illegal combatants ❀◕ ‿ ◕❀

Pogchamping as Seymour Hersh cites anonymous Israeli sources

1·15 hours ago

1·15 hours agoYou’re already easy for me to dislike but now I’ve got to kill you

Kadyrov declares open season on the NATOids

Holy shit it’s ousted sex pest Alexander Reid Ross! How have you been?

Hell yeah

9·28 days ago

9·28 days agogeorg lukacs

samir amin

domenico losurdo

michael hudson

zhang yibing

read the ones they cite and you will be Somewhere

I was logged-off for almost 4 days identifying berrylike fruiting bodies of lichen when I learned Iran proved me right as I always have been

{kind=link}

{kind=link}

1·28 days ago

1·28 days agodeleted by creator

Ping me too next time if you don’t mind